Loading NuWatt Energy...

We use your location to provide localized solar offers and incentives.

We serve MA, NH, CT, RI, ME, VT, NJ, PA, and TX

Loading NuWatt Energy...

NuWatt designs, installs, and manages solar, battery, heat pump, and EV charger systems across 9 states. One company, one warranty, one point of contact.

Get a Free Quote

The residential solar tax credit is dead. But the investment tax credit is alive — and it's how solar leases, PPAs, and NuWatt's Propel program still deliver federal tax savings to your roof. This is the definitive guide to how it works, what it saves you, and how new starts qualify by being placed in service by December 31, 2027.

$0

Homeowner ITC

25D expired

30%

TPO ITC Rate

48/48E active

20–40%

Your Savings

lower monthly

Dec 31, 2027

In Service By

new starts

The Section 48/48E begin-construction safe harbor closed July 4, 2026. Projects that began construction on or before that date locked in the longer timing pathway; new lease, PPA, and Propel projects still qualify for the 30% Investment Tax Credit but generally must be placed in service by December 31, 2027. Permitting alone takes 4-8 weeks, so plan your timeline accordingly.

You cannot claim the credit yourself (Section 25D expired). But if a financing company owns the solar system on your roof through a lease, PPA, or Propel agreement, that company claims the 30% Investment Tax Credit under Section 48/48E and passes the savings to you as lower monthly payments. The begin-construction safe harbor closed July 4, 2026; new projects still qualify but generally must be placed in service by December 31, 2027.

Section 48/48E is the path forward for homeowners in any of these situations:

You want solar but missed the Section 25D deadline (expired Dec 31, 2025)

You don't have enough federal tax liability to use a direct credit anyway

You prefer $0 down with no large upfront costs

You're in a high-rate state and want to lock in lower energy costs today

You want ownership eventually — Propel transfers the system to you at year 5

Section 48 of the Internal Revenue Code has existed since 1962. It provides an Investment Tax Credit (ITC) to the owner of a qualifying energy system — solar panels, battery storage, wind turbines, and more. Section 48E, created by the Inflation Reduction Act in August 2022, extended and expanded this credit with technology-neutral clean energy rules.

The critical word is "owner." Section 48/48E does not care whether the solar system sits on a commercial warehouse or your residential rooftop. It only cares who owns it. If a business entity owns the system, that entity claims the 30% credit on IRS Form 3468.

This is the legal mechanism that makes solar leases, PPAs, and programs like NuWatt's Propel work in 2026. A financing company purchases the solar system, installs it on your roof, claims the 30% ITC and MACRS depreciation, and passes those savings to you through lower monthly payments or a reduced per-kWh rate.

This is not a loophole. Congress designed Section 48/48E specifically to encourage solar deployment by any entity that can use the credit — including third-party residential solar providers.

Understanding the difference between these two tax code sections is the key to unlocking solar savings in 2026.

| Section 25D (Dead) | Section 48/48E (Active) | |

|---|---|---|

| Who claims it | The homeowner (you) | The system owner (financing company) |

| Credit rate | 30% (was) | 30% (still active) |

| Current status | EXPIRED Dec 31, 2025 | ACTIVE — July 4, 2026 was the begin-construction safe-harbor date, not an expiry |

| Applies to | Systems you buy with cash or loan | Systems owned by a business entity (lease, PPA, Propel) |

| IRS form | Form 5695 (residential) | Form 3468 (investment credit) |

| MACRS depreciation | Not available to homeowners | 5-year accelerated + 100% first-year bonus (permanent under OBBBA) |

| How you benefit | Direct dollar-for-dollar credit on your taxes | Lower lease/PPA payments (owner passes savings to you) |

| Timing | OBBBA (July 4, 2025) — expired Dec 31, 2025 | Projects that began construction on or before July 4, 2026 locked in the full timing pathway; later starts still qualify but must be placed in service by Dec 31, 2027 |

Section 25D let you claim the credit on your tax return. Section 48/48E lets a business entity claim the credit — and that business passes the savings to you through lower lease/PPA payments. You never file IRS Form 3468 yourself.

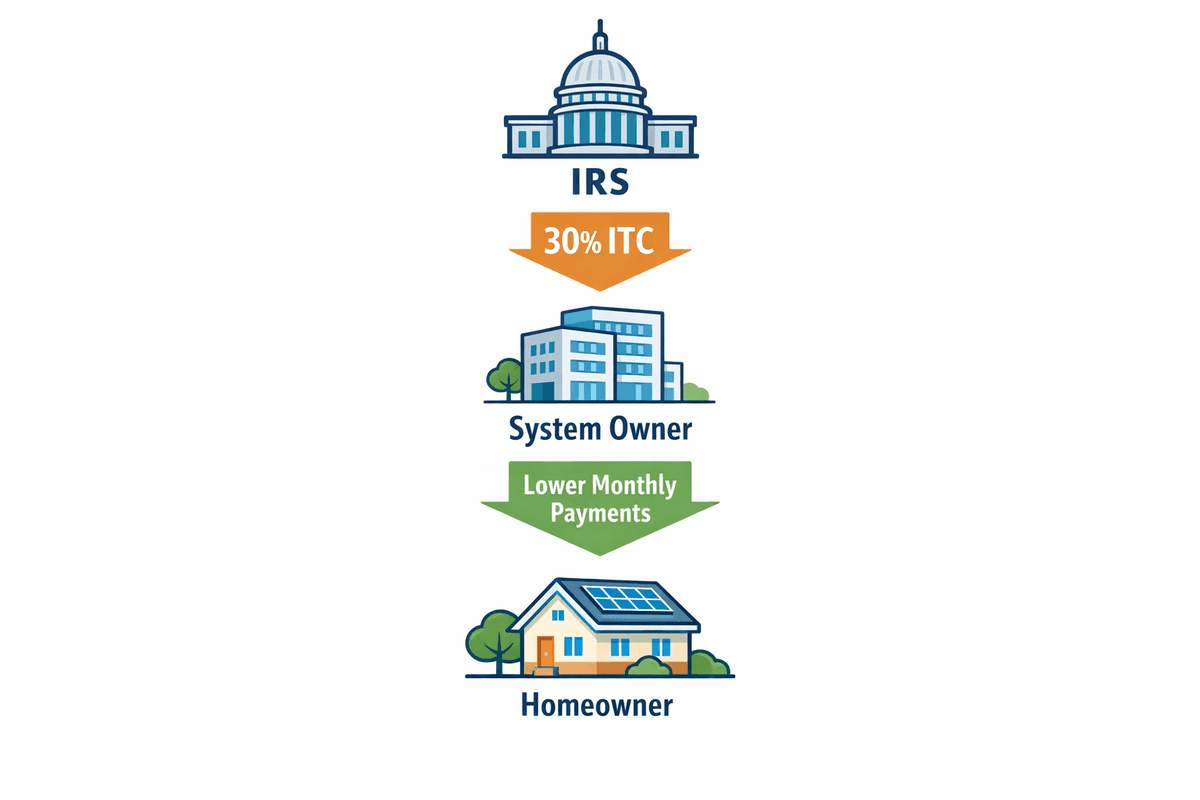

Follow the path of the 30% ITC from the federal government to your monthly savings. Based on a typical $28,000 residential solar system.

Purchases your solar system for $28,000 and installs it on your roof

Issues the 30% ITC to the system owner via IRS Form 3468

Claims MACRS depreciation (5-year accelerated schedule + 100% first-year bonus, permanent under OBBBA)

Passes the combined tax savings to you through lower monthly lease/PPA payments

Pay a locked-in monthly rate below your current electric bill. Save from day 1.

All three options use the same Section 48/48E mechanism. The difference is how the savings reach you and whether you eventually own the system.

How the ITC reaches you

TPO claims 30% ITC → uses it to set a lower fixed monthly payment for you

Payment type

Fixed monthly payment (e.g., $120/mo)

Escalator

2–3% annual increase (typical)

Ownership

Never — TPO owns for full term (20–25 years)

Maintenance

Included — TPO handles everything

ITC savings to you

Baked into the lower monthly rate — you never see the ITC directly

Best for

Homeowners who want predictable payments and zero hassle

How the ITC reaches you

TPO claims 30% ITC → uses it to offer you a below-market $/kWh rate

Payment type

Pay per kWh produced (e.g., $0.12/kWh)

Escalator

0–2.9% annual increase (varies by provider)

Ownership

Never — TPO owns for full term (20–25 years)

Maintenance

Included — TPO handles everything

ITC savings to you

Reflected in your locked-in rate being well below utility prices

Best for

Homeowners in high-rate states who want the lowest $/kWh

How the ITC reaches you

TPO claims 30% ITC for years 1–5 → transfers ownership to you at year 5

Payment type

Fixed monthly loan payment (e.g., $155/mo)

Escalator

None — fixed for 25-year loan term

Ownership

You own from year 5 onward (no buyout fee)

Maintenance

Included years 1–5, then your responsibility

ITC savings to you

ITC + MACRS reduce your effective system cost by ~35%, lowering your monthly payment

Best for

Homeowners who want ITC savings AND long-term ownership

These are real-world scenarios based on current market rates. The 30% ITC is the reason these monthly payments are achievable.

System cost

$28,000 (paid by owner)

ITC value

$8,400 (claimed by owner)

Your monthly savings

$90–$150/mo vs. electric bill

Year 1 savings

$1,080–$1,800

25-year total savings

$27,000–$45,000

Payback period

Immediate — savings start day 1

System cost

$32,000 (paid by owner)

ITC value

$9,600 (claimed by owner)

Your monthly savings

$70–$120/mo vs. electric bill

Year 1 savings

$840–$1,440

25-year total savings

$21,000–$36,000

Payback period

Immediate — pay-per-kWh below utility rate

System cost

$29,500 (paid by owner, then transfers to you)

ITC value

$8,850 (claimed by owner, baked into your lower payment)

Your monthly savings

$60–$100/mo vs. electric bill

Year 1 savings

$720–$1,200

25-year total savings

$38,000–$50,000 (you own from year 5)

Payback period

Immediate savings, full ownership at year 5

There is enormous confusion about what happened to solar tax credits. Here are the facts.

Myth: There is no solar tax credit in 2026.

Fact: The homeowner credit (Section 25D) expired, but the investment credit (Section 48/48E) is alive. Third-party owners claim the 30% ITC and pass savings to you through a lease, PPA, or Propel agreement.

Myth: Solar leases are a scam — the company keeps all the tax credit.

Fact: The company claims the ITC because it legally owns the system. But the ITC is the reason your monthly payment is 20–40% lower. Without the ITC, your lease/PPA rate would be significantly higher. The savings are passed through to you — that's the entire business model.

Myth: My solar installer gets the tax credit.

Fact: Installers do not claim the ITC. The credit goes to the system OWNER. In a lease or PPA, the owner is the financing company (e.g., Sunrun, Sunnova, or the entity behind NuWatt's Propel program). NuWatt is the installer; the TPO partner is the owner.

Myth: I need to file special tax forms to benefit from Section 48/48E.

Fact: You file nothing. The third-party owner handles all IRS filings (Form 3468). You simply sign a lease/PPA agreement and pay your monthly bill. The tax benefit is already built into your rate.

Myth: Buying solar is always better than leasing.

Fact: Before 2026, cash buyers got the same 30% credit AND owned the system — making buying clearly superior. Now that homeowners get $0 credit, leases and PPAs are financially competitive. In high-rate states, a PPA with the 30% ITC pass-through can save more than a cash purchase over the first 10 years.

Myth: Section 48E is only for commercial buildings.

Fact: Section 48E applies to any entity that owns a qualifying clean energy system. There is no restriction against placing the system on a residential rooftop. The credit goes to the business owner, and the electricity benefits the homeowner.

Myth: I should wait until 2027 when the tax credit might come back.

Fact: There is zero indication that Congress will reinstate Section 25D. The OBBBA explicitly killed it. Meanwhile, July 4, 2026 was the Section 48/48E begin-construction safe-harbor date: projects that began construction on or before it locked in the full timing pathway (placed in service through roughly 2030), and projects that begin later still qualify but generally must be placed in service by December 31, 2027. Section 25D, by contrast, is gone for homeowner purchases — so a lease/PPA/Propel is the only path to the credit.

If the system owner sells or disposes of the solar system within 5 years of placing it in service, the IRS "recaptures" a portion of the ITC. The recapture amount decreases by 20% each year. This is why lease and PPA terms are typically 20–25 years — and why Propel's ownership transfer happens at year 5 (after the recapture period ends).

| Disposition Year | Recapture Amount |

|---|---|

| Year 1 | 100% of ITC recaptured |

| Year 2 | 80% recaptured |

| Year 3 | 60% recaptured |

| Year 4 | 40% recaptured |

| Year 5 | 20% recaptured |

| Year 6+ | $0 — no recapture |

This is exactly why Propel transfers ownership at year 5 — the recapture risk is zero, and the system is yours free and clear.

To qualify for the full 30% ITC (instead of 6%), the system owner must pay installers prevailing wages and meet apprenticeship requirements. As a homeowner, this doesn't directly affect you — the financing company handles compliance. But it means your installer's labor costs may be slightly higher, which is already factored into your lease/PPA rate.

Full 30% credit requires prevailing wage + apprenticeship compliance

Without compliance, the credit drops to just 6% — making leases/PPAs much less attractive

NuWatt and its TPO partners comply with prevailing wage requirements on all installations

Your lease/PPA rate already accounts for any additional labor costs from compliance

The Foreign Entity of Concern (FEOC) rules restrict which components can be used in ITC-eligible projects. Starting in 2026, at least 40% of manufactured components must come from non-FEOC countries (not China, Russia, Iran, or North Korea). This primarily affects the financing company's component selection, not you.

FEOC restrictions apply to panels, inverters, batteries, and racking

2026 threshold: 40% non-FEOC content (rising to 50% in 2027)

Qualifying domestic manufacturers: First Solar, Qcells, Silfab, Enphase, SolarEdge

NuWatt uses FEOC-compliant equipment on all TPO installations to protect ITC eligibility

Here is how the Section 48/48E timing works now — and what it means for qualifying your project for the 30% ITC.

Understanding your options takes 1–2 weeks. Starting now gives maximum flexibility for equipment selection and scheduling.

Permitting and utility interconnection take 4–8 weeks. Projects that began construction on or before July 4, 2026 locked in the full Section 48/48E timing pathway; new starts still qualify but must be placed in service by December 31, 2027.

"Begin construction" means physical work starts OR 5% of project costs are incurred. Documenting this on or before July 4, 2026 locked in the full timing pathway; later starts still qualify but must be placed in service by Dec 31, 2027.

Beginning construction on or before this date locked in the full Section 48/48E timing pathway (placed in service through roughly 2030). Projects that begin later still qualify for the 30% ITC but generally must be placed in service by December 31, 2027 — a tighter window, plus rising equipment and tariff costs make earlier starts the safer bet.

Section 48/48E works in every state, but monthly costs and local incentives vary. Here is what is available in the states NuWatt serves.

| State | Lease | PPA | Propel | Typical Monthly | Notes |

|---|---|---|---|---|---|

| Massachusetts | Coming soon | $100-$170/mo | SMART 3.0 adds $0.03/kWh on top. Eversource $0.28/kWh makes PPA very competitive. | ||

| Connecticut | Coming soon | $90-$150/mo | No state solar rebate. High utility rates make lease/PPA attractive. | ||

| Rhode Island | Coming soon | $85-$140/mo | $0.65/W REF rebate stacks. REG program adds $0.27/kWh for 15-20 years. | ||

| New Hampshire | Coming soon | $95-$155/mo | No state rebate (repealed 2024). NEM 2.0 credits ~85% of retail. | ||

| Vermont | Coming soon | $90-$145/mo | Net metering at 1:1 retail. Lower rates ($0.21/kWh) mean longer payback. | ||

| Maine | Yes | $80-$135/mo | Propel available. 1:1 net billing for rooftop. CMP $0.27/kWh, Versant $0.32/kWh. | ||

| New Jersey | Coming soon | $85-$140/mo | ADI $85.00/MWh adds performance income. High SREC value. | ||

| Pennsylvania | Coming soon | $80-$130/mo | Moderate rates (~$0.17/kWh). SRECs available in some areas. | ||

| Texas | Yes | $75-$125/mo | Propel available. Deregulated market. Austin Energy has local rebates. |

SMART 3.0 adds $0.03/kWh on top. Eversource $0.28/kWh makes PPA very competitive.

No state solar rebate. High utility rates make lease/PPA attractive.

$0.65/W REF rebate stacks. REG program adds $0.27/kWh for 15-20 years.

No state rebate (repealed 2024). NEM 2.0 credits ~85% of retail.

Net metering at 1:1 retail. Lower rates ($0.21/kWh) mean longer payback.

Propel available. 1:1 net billing for rooftop. CMP $0.27/kWh, Versant $0.32/kWh.

Moderate rates (~$0.17/kWh). SRECs available in some areas.

Propel available. Deregulated market. Austin Energy has local rebates.

Not seeing your state? Section 48/48E works nationwide. The states above are where NuWatt currently provides installation services. Monthly costs depend on system size, local utility rates, and available state incentives.

Section 48/48E is the last federal mechanism for homeowners to access solar tax savings. Its begin-construction safe harbor closed July 4, 2026; new projects still qualify but generally must be placed in service by December 31, 2027. Start your assessment today.

NuWatt Energy is a licensed solar installer serving MA, CT, RI, NH, ME, VT, NJ, PA, and TX. Propel is currently available in ME and TX.