Loading NuWatt Energy...

We use your location to provide localized solar offers and incentives.

We serve MA, NH, CT, RI, ME, VT, NJ, PA, and TX

Loading NuWatt Energy...

NuWatt designs, installs, and manages solar, battery, heat pump, and EV charger systems across 9 states. One company, one warranty, one point of contact.

Get a Free QuoteSection 25D is dead. If you buy solar with cash or a loan, you get $0 from the IRS. But Section 48E lets third-party financing companies still claim the 30% ITC — and pass those savings to you through lower lease payments, PPA rates, and ESA terms. Here is exactly how it works, state by state.

30%

Section 48E ITC

DEAD

Section 25D

$50-150/mo

Lease Savings

Jul 4, 2026

Window Closed

The Section 48E begin-construction window closed July 4, 2026: projects that began construction on or before that date locked in the full timing pathway (placed in service through roughly 2030). Commercial solar projects starting now still qualify for the 30% credit, but generally must be placed in service by December 31, 2027. For homeowners, the residential Section 25D credit expired December 31, 2025 — the only way to reach the 30% credit now is through a third-party-owned lease, PPA, or ESA, where the financing company owns the system, claims Section 48E, and passes the savings through lower rates.

Two tax code sections, two very different fates

On July 4, 2025, the OBBBA (One Big Beautiful Bill Act) was signed into law. It eliminated Section 25D— the residential solar investment tax credit that had given homeowners up to 30% back on solar purchases since 2005.

Before the OBBBA, a homeowner who installed an 8 kW solar system for $25,200 could claim a $7,560 federal tax credit on their personal return. That era is over. If you buy solar with cash or a loan in 2026, you receive $0 from the IRS.

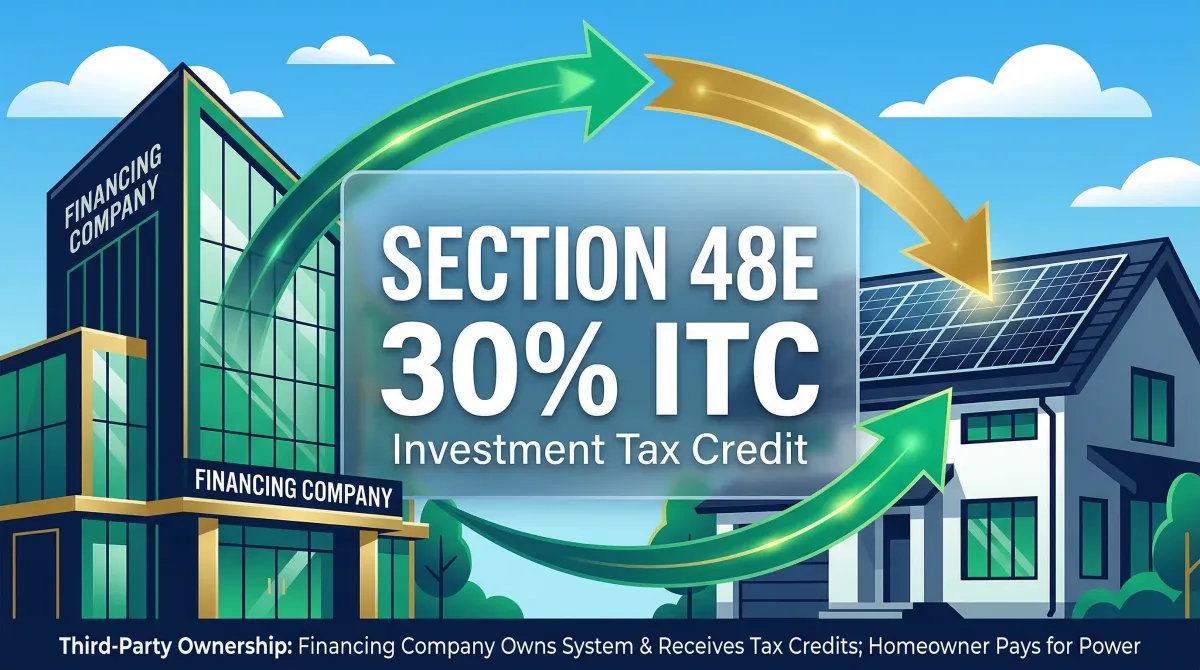

But Congress left another pathway intact: Section 48E. This provision (originally Section 48, in place since 1962) provides the same 30% ITC, but to the business entitythat owns the energy property. For residential solar, this means the financing company that owns a leased or PPA system can still claim the full credit — and pass those savings to homeowners.

The financing company owns the panels. You get the savings.

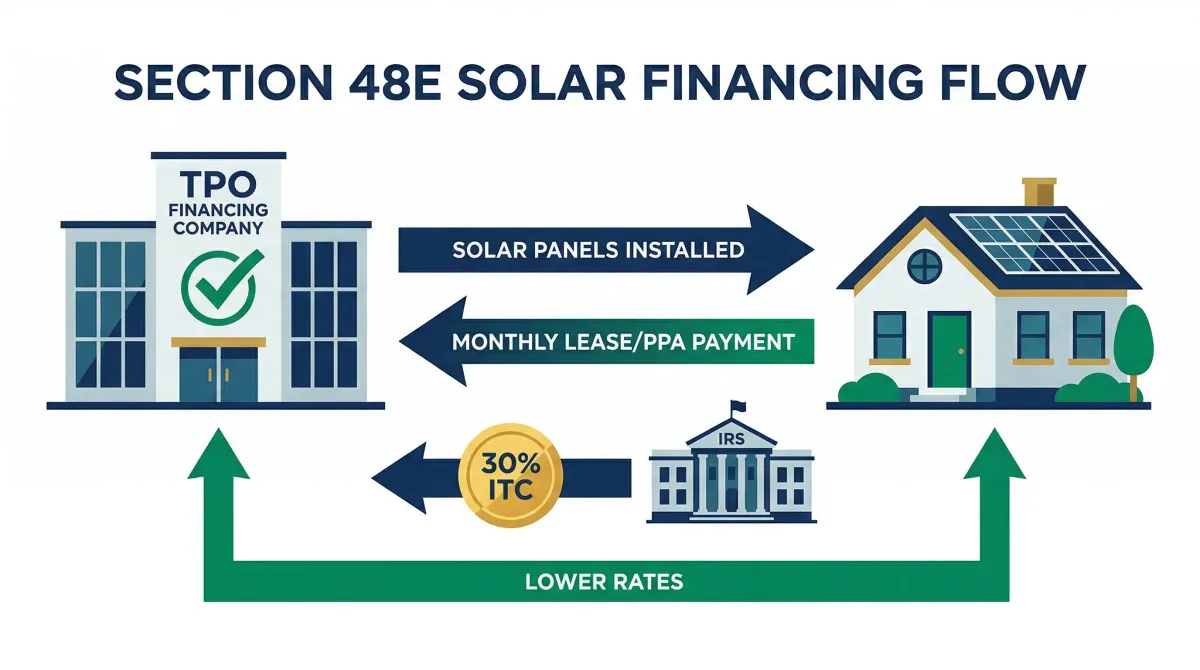

With a solar lease or PPA, you do not own the panels. A financing company (called a third-party owner, or TPO) purchases the system, hires a contractor like NuWatt to install it on your roof, and owns it for the contract term. Because the TPO owns the system, they claim Section 48E benefits. Here is how the money flows:

A financing company buys a solar system (e.g., 8 kW at ~$3.00/W = ~$24,000). They contract with NuWatt to install it on your roof. The TPO owns the panels, inverter, and mounting hardware.

The TPO files IRS Form 3468 and claims the 30% Investment Tax Credit (~$7,200 on a $24,000 system). This goes to the financing company — not to you, and not to the installer. The operative word in the tax code is "owner."

The TPO also claims MACRS (Modified Accelerated Cost Recovery System) depreciation. Under OBBBA, 100% first-year bonus depreciation was permanently restored, so the entire depreciable basis (~$20,400 after the ITC basis reduction on our $24,000 example) is deducted in year one. Additional benefit: ~$4,300 at a 21% corporate rate.

The combined ~$11,500 in tax benefits (ITC + MACRS) reduces the TPO cost basis by ~48%. Competition among TPOs forces them to pass this to you through lower lease payments ($80-140/mo) or discounted PPA rates ($0.08-0.15/kWh).

Your lease/PPA payment is lower than your previous electric bill. You save money from the first month. The TPO handles maintenance, monitoring, and warranties for the contract term (typically 20-25 years).

Base ITC

Standard investment tax credit for all qualifying solar systems

Domestic Content (FEOC)

Equipment manufactured in the USA; must meet FEOC requirements

Energy Community

Project sited in a coal community, brownfield, or high-fossil-employment area

Low-Income / Indian Country

Projects in low-income communities or on tribal lands

Most residential TPO projects qualify for 40-50% with the domestic content adder. The maximum theoretical credit is 70%.

Beginning construction bythis date — not completing it — locked in the full timing pathway

Section 48E has two timing pathways. Projects that began constructionon or before July 4, 2026 locked in the full timing pathway (placed in service through roughly 2030). Projects that begin construction after that date can still qualify, but generally must be placed in service by December 31, 2027. Beginning construction does not mean the project must be finished — just that meaningful work has started. The IRS recognizes two safe harbors:

Meaningful physical work begins at the project site or on equipment. This includes mounting hardware fabrication, racking installation, or panel delivery to the site.

At least 5% of total project cost has been incurred. For a $24,000 system, that means $1,200+ in equipment orders or deposits. Projects must then be placed in service within 4 years.

Answer two questions to see your governing deadline.

“Begin construction” means the IRS Physical Work Test or the 5% Safe Harbor — not project completion.

Qualifies — if placed in service in time

Pathway B — construction begins after July 4, 2026

Your project still qualifies for the 30% Section 48E credit (plus any adders), but because construction begins after the safe-harbor date it must be placed in service by December 31, 2027. Permitting, equipment procurement, and interconnection are the critical path — build the schedule backward from that date.

Governing deadline: placed in service by December 31, 2027.

Decision helper only — confirm eligibility with your tax advisor and developer. Section 48E remains active on two pathways; the begin-construction safe-harbor window closed July 4, 2026, and projects starting after it must be placed in service by December 31, 2027.

Jul 4, 2025

Section 25D residential credit eliminated. Section 48E commercial credit preserved with construction deadline.

Dec 31, 2025

Last day for homeowners to claim the residential ITC on systems placed in service. $0 federal credit for cash/loan buyers after this date.

Jan 1, 2026

Solar purchases with cash or loan receive no federal tax credit. Third-party owned systems (lease/PPA) still qualify under Section 48E.

Today

Sign a lease/PPA agreement so the TPO can begin construction (order equipment, pay 5%+ of project cost) and place the system in service by December 31, 2027.

Jul 4, 2026

Projects that began construction (Physical Work Test or 5% Safe Harbor) on or before this date locked in the full timing pathway, placed in service through roughly 2030. Projects beginning construction after this date can still qualify but generally must be placed in service by December 31, 2027.

State incentives stack with 48E to create dramatically different economics

Section 48E is a federal benefit, but the impact varies enormously by state. States with high electricity rates and strong state-level incentives see the biggest savings from third-party solar ownership.

State Incentive:

SMART 3.0 ($0.03/kWh, 20 yr)

Why 48E wins here: Highest electric rates + SMART income = best TPO economics in nation

State Incentive:

ADI $85.00/MWh (15 yr)

Why 48E wins here: ADI payments go to TPO, reducing your lease/PPA rate further

State Incentive:

RRES netting + sales tax exempt

Why 48E wins here: RRES net metering + 48E makes lease savings immediate

State Incentive:

REG 31.55¢/kWh OR REF $0.65/W (pick one)

Why 48E wins here: Whichever state track (REG or REF) the TPO chooses stacks powerfully with 48E

State Incentive:

NEM 2.0 (~85% retail credit)

Why 48E wins here: No state rebate means 48E is the only federal-level benefit left

State Incentive:

1:1 net metering + tax exempt

Why 48E wins here: 1:1 net metering + property/sales tax exempt + 48E

State Incentive:

SRECs (limited market)

Why 48E wins here: Lower rates make ownership less attractive; lease/PPA reduces risk

State Incentive:

Net metering + sales tax exempt

Why 48E wins here: Moderate rates + no state solar rebate = 48E matters more

State Incentive:

No state incentive; low cost + high sun

Why 48E wins here: Lowest cost per watt in the country; 48E makes PPA rates extremely competitive

Everything above covers third-party-owned residential solar. If your organisation owns the system directly, you claim Section 48E yourself — and if you pay no federal tax, you monetise it through elective pay or by transferring the credit.

How the math changed when Section 25D died

Before 2026, cash and loan buyers had a clear advantage: the 30% tax credit. Now that 25D is gone, the financing landscape has fundamentally shifted. Lease and PPA options are now more competitive for most homeowners.

| Category | Cash | Loan | Lease | PPA |

|---|---|---|---|---|

| Upfront Cost | $24,000-30,000 | $0 down | $0 down | $0 down |

| Monthly Payment | $0 | $180-280/mo | $80-140/mo | Per kWh used |

| Federal Tax Credit | $0 (25D dead) | $0 (25D dead) | 30% via 48E | 30% via 48E |

| Effective $/W | $2.85-3.15/W | $2.85-3.15 + interest | ~$2.00-2.20/W (TPO) | ~$2.00-2.20/W (TPO) |

| You Own System | Yes, day 1 | Yes, day 1 | No (TPO owns) | No (TPO owns) |

| State Incentives | You keep 100% | You keep 100% | TPO typically claims | TPO typically claims |

| Maintenance | You handle | You handle | TPO handles | TPO handles |

| Rate Lock | $0 electricity | Fixed loan payment | Fixed lease rate | Locked $/kWh rate |

| 25-Year Total Savings | $50K-95K | $35K-70K | $20K-45K | $25K-50K |

| Payback Period | 10-15 yr (no ITC) | 12-17 yr (no ITC) | Day 1 savings | Day 1 savings |

| Best For | Long-term investors | Ownership priority | Predictable bills | Max day-1 savings |

Based on national averages for an 8 kW residential system. Actual figures vary by state, utility rate, system size, and TPO company. All numbers reflect 2026 post-25D expiration economics.

Requirements for solar leases, PPAs, and ESAs

You do not need to qualify for the tax credit yourself — the TPO does that. But you need to qualify for the lease or PPA agreement. Here are the typical requirements:

You must own the home where the system is installed. Renters cannot sign a lease/PPA on a property they do not own.

Your roof should have 15+ years of remaining life. Most TPOs require a roof inspection. If a reroof is needed, do it before solar.

Most TPO companies require 650+ (some accept 600+). This is lower than traditional solar loans because the TPO owns the asset as collateral.

Your roof needs adequate solar access. South, east, or west-facing roofs work. Heavy shading from trees or buildings may disqualify a property.

Most TPOs require a minimum electric bill of $75-100/month. Higher bills = more savings. The sweet spot is $150+/month.

You must be in a utility territory that allows net metering or has favorable interconnection rules. Most Northeast utilities qualify.

Separating fact from fiction in the post-25D landscape

“The solar tax credit is completely gone in 2026.”

The residential credit (Section 25D) is dead. But the commercial credit (Section 48E) is alive and available through third-party ownership models like leases, PPAs, and ESAs.

“Only businesses can benefit from Section 48E.”

Only businesses can claim the credit directly. But homeowners benefit indirectly when a TPO company claims 48E and passes savings through lower lease/PPA rates.

“Solar installers claim the Section 48E credit.”

The system OWNER claims the credit, not the installer. The installer (like NuWatt) designs and installs. The financing company (TPO) owns the system and claims 48E.

“You need perfect credit to get a solar lease or PPA.”

Most TPO companies require a credit score of 650+, though some go as low as 600. A solar lease has a lower credit threshold than a traditional solar loan because the TPO owns the asset.

“Solar leases and PPAs are scams.”

Legitimate leases and PPAs are legal contracts regulated by state utility commissions. The key is understanding the terms: escalator rates, end-of-term options, and transfer clauses. Read before you sign.

“The 30% credit will come back for homeowners eventually.”

There is no scheduled restoration of Section 25D. The OBBBA (signed July 4, 2025) eliminated it with no sunset clause. Waiting for it to return means paying full utility rates in the meantime.

“Cash purchase is always better than leasing.”

Before 2026, cash buyers got a 30% tax credit. Now they get $0. A cash purchase still yields higher 25-year savings, but requires $24K-30K upfront with no federal offset. For most homeowners, a lease or PPA now provides better risk-adjusted returns.

“Section 48E has no timing rules.”

There are two pathways. Projects that began construction on or before July 4, 2026 preserved the full Section 48E timing pathway (placed in service through roughly 2030). Projects that begin construction after that date can still qualify, but generally must be placed in service by December 31, 2027. The IRS defines "begin construction" through two safe harbors: the Physical Work Test or the 5% Safe Harbor.

“TPO companies pocket the entire 48E credit.”

Competition among TPOs forces them to pass savings to homeowners. The 30% ITC + MACRS depreciation reduces the TPO cost basis by ~45%, which is why lease payments ($80-140/mo) are dramatically lower than loan payments ($180-280/mo).

“A solar lease hurts your home value.”

Studies show solar homes sell for 3-4% more regardless of ownership model. Most leases are transferable to the new buyer. The key is disclosing the lease during the sale process and ensuring the buyer qualifies for transfer.

12 questions every homeowner is asking in 2026

Section 48E (formerly Section 48) is the commercial/investment tax credit for businesses that own energy-generating property. Section 25D was the residential tax credit for individual homeowners. Section 25D expired December 31, 2025. Section 48E remains active: projects that began construction on or before July 4, 2026 preserved the full timing pathway (placed in service through roughly 2030), and projects that begin construction after that date can still qualify but generally must be placed in service by December 31, 2027. The key difference: 48E can only be claimed by the entity that owns the system (a business), not the homeowner.

Not directly. Homeowners who buy solar with cash or a loan receive $0 in federal tax credits in 2026. However, homeowners can benefit indirectly through a solar lease, PPA, or Energy Service Agreement (ESA) where a third-party financing company owns the system, claims the 30% Section 48E ITC, and passes savings through lower rates.

There are two pathways, both of which preserve the credit. Projects that began construction on or before July 4, 2026 preserved the full Section 48E timing pathway (placed in service through roughly 2030). Projects that begin construction after that date can still qualify, but generally must be placed in service by December 31, 2027. The IRS defines "begin construction" through two safe harbors: (1) Physical Work Test — meaningful physical work begins at the site, or (2) Five Percent Safe Harbor — at least 5% of total project cost has been incurred.

A TPO is a financing company that purchases and owns solar equipment installed on your property. Because they own the system, they claim the Section 48E ITC and MACRS depreciation. You benefit through a lease (fixed monthly payment), PPA (pay per kWh generated), or prepaid ESA (one-time payment, ownership transfers after term). Common TPOs include Sunrun, Sunnova, and various regional financing companies.

Solar lease payments range from $80-140/month nationally for a typical 8 kW residential system in 2026. The exact amount depends on your state, utility rate, system size, and the TPO company. Compare this to average electric bills of $150-300+/month in the Northeast. Most homeowners save $50-150/month from day one.

A solar lease charges a fixed monthly payment regardless of production. A PPA (Power Purchase Agreement) charges per kilowatt-hour of electricity generated, typically $0.08-0.15/kWh. Both require $0 down, both are maintained by the TPO, and both benefit from Section 48E. Leases offer more predictable budgeting; PPAs can save more during high-production months.

Yes, for most homeowners. Through a lease or PPA, you still benefit from Section 48E indirectly. Even for cash buyers, solar pays back in 10-15 years in high-rate states (MA, RI, CT, NH, NJ, ME) due to high electricity costs and state incentives. The math is worse in low-rate states (TX, PA) for cash buyers but still positive for lease/PPA customers.

At the end of a typical 20-25 year lease, you have three options: (1) Renew the lease at a reduced rate, (2) Purchase the system at fair market value (usually very low after 20+ years), or (3) Have the TPO remove the system at no cost. Most homeowners purchase the system for a nominal amount.

Yes. Most solar leases are transferable to the new homeowner. The buyer must meet the TPO credit requirements (typically 650+ score). Some TPOs allow a buyout at sale. Disclosure of the lease obligation is required in the real estate transaction.

Section 48E has several bonus adders: +10% for domestic content (FEOC-compliant equipment), +10% for siting in an energy community, and +10-20% for low-income community or Indian Country projects. The maximum possible credit is 70%. Most residential TPO projects qualify for 40-50% with the domestic content adder.

No. There is no scheduled restoration of Section 25D. The OBBBA eliminated it without a sunset clause. Meanwhile, Section 48E timing tightens after July 4, 2026: projects that began construction on or before that date kept the full timing pathway (placed in service through roughly 2030), while projects beginning construction after it generally must be placed in service by December 31, 2027. Waiting narrows your window and means paying full utility rates in the meantime.

States with the highest electricity rates and strongest state incentives benefit most: Massachusetts (SMART 3.0 + $0.29/kWh rates), Rhode Island (REG or REF — pick one — + $0.29/kWh), Connecticut ($0.27/kWh + RRES), and New Jersey (ADI program + $0.26/kWh). These states see lease/PPA savings of $1,000-1,800+ in year one alone.

Complete guide to solar leasing and PPAs in the post-25D era.

State-by-state analysis of whether solar is still worth it.

Deep dive into how 48E works for residential solar customers.

Honest math on solar payback periods and savings without 25D.

The real answer: it depends on your state, rate, and financing.

Foreign Entity of Concern rules and the July 4, 2026 deadline.

Side-by-side comparison now that 25D is gone.

Everything that changed with the OBBBA and what still works.

Timeline and safe harbor rules for the July 4, 2026 deadline.

Get a free, no-obligation solar assessment from NuWatt. We will evaluate your roof, utility rate, and state incentives — and show you exactly what a lease, PPA, or Propel ESA would cost with Section 48E benefits.

Or call us: 877-772-6357